Payments | Case study of payments challenges in Pacific Islands

Payment infrastructure in the Pacific Islands lags behind the global average. In this article we’ll detail the reasons why that is the case, the impact it has, what the future holds, and how you can start to take action today to level the playing field.

Pacific Islands merchants are suffering high charged fees

The global average retail fee that a merchant is charged to take a card payment is 3.5%. However, the average retail fee that a merchant is charged to take a card payment in the Pacific Islands is 7.5%

Current Pacific Islands Payment Infrastructure

The biggest reason for the gap between payment fees in the Pacific Islands compared to the rest of the world is due to the fact that there is no local Acquirer in the Pacific Islands.

Without a local acquirer to facilitate and offer merchant services, businesses have had to look outside of the Pacific Islands and most commonly tried to obtain a partnership with a bank in Australia or New Zealand. While some businesses in the Pacific have found success and been granted a solution with one of these banks, this is far from perfect.

There is no local acquirer in Pacific Islands, which forces the local businesses to seek merchant services overseas.

For a start, these banks do not have a product specifically designed for merchants outside of their countries to use. So this means that any merchant in the Pacific has to settle their transaction in Australian or New Zealand dollars, and then take it upon themselves to transfer that money to their own local currency…accruing further excessive fees.

Secondly, due to the much lower amount of transaction volume in the Pacific Islands compared to what the banks see in Australia or New Zealand, the banks are not concerned or focused on trying to build a more tailored solution for this. They see the Pacific Islands as an extremely high-risk region. As a result, they have installed high financial bonds, up to and over $30,000, that are required to get the process started for a business to get a payment facility.

If a business is able to come up with this bond, not to mention this is now money the business can’t use, they will now have to go through an excruciating and lengthy onboarding process that can take up to 9 months before they are able to take their first transaction.

Impact on Merchants

Not having a local acquirer in the region causes many negative situations – all leading to lower commerce and revenue not only for the individual businesses but the country’s economies as a whole.

-

Not being able to get a merchant account due to large financial bonds required

-

Lengthy process for onboarding and setup

-

Extremely high fees

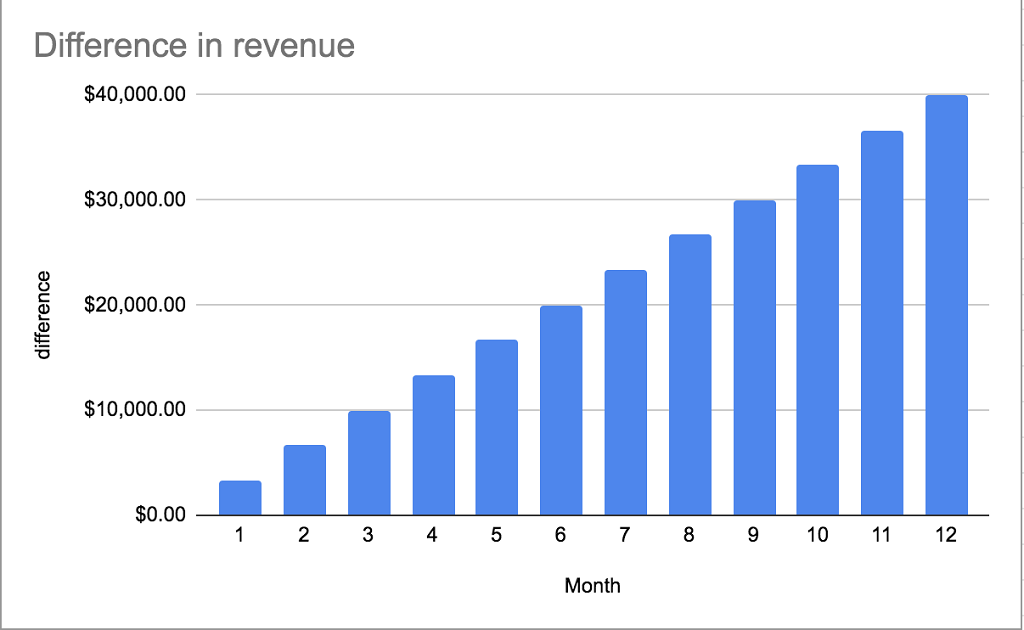

Here is a chart that shows the financial impact on a business from the current fees being charged for payments in the Pacific Islands.

For a merchant with an average revenue of $1million from card payments per year, the difference in revenue for one year at the global average of 3.5% vs the current Pacific average of 7.5% is $40,000.

The Future

The good news is that things are quickly changing in the global payment landscape, with new technologies and players innovating ways to open up easier and more affordable alternatives. Large global acquirers such as Fiserv, Adyen, Stripe are always expanding their reach into which countries they are able to operate locally and have already started the conversations for setting up in the Pacific Islands.

Getting a local acquirer is still likely 3+ years away, so finding immediate impact before that is of course what everyone wants. A new wave of companies that focus on providing merchant solutions to emerging markets and regions with no local acquirers now starting to arise. Companies such as Kovena, who partner with multiple acquirers and FX disbursement companies globally are able to leverage the large number of volumes that they transact in order to negotiate lower rates from these partners and pass the savings onto the merchants. Instead of sending $100 dollars overseas at a time with a $10 fee, these companies send billions throughout the year. You can understand why they are able to bring the rates down.

Another space that is expanding rapidly is the industry-specific payment space. Companies such as Hotel Link, which only operate in one vertical (in this case accommodation) have an immense amount of data about their industry. Currently, banks and acquirers have a “one size fits all” approach to offering merchant solutions, which means they give the same fee and risk profiles for most businesses…even if it is a grocery store versus someone who sells diamonds out of the back of their car. With a specialised approach, these industry-specific players can tailor their fees and operations to run as efficiently and low as possible.

How to take action

Hotel Link has recently launched a new digital payment solution, Hotel Link Pay, which is empowered by Kovena to offer accommodation providers an optimal alternative to the in-house payment method applied. Our solution will simplify the payment process for your guests and improve your own workflow.

Secure, Convenient and Finance Beneficial are all gains that you can have when applying Hotel Link Pay. Contact us for more details.

Relative Posts

Payments | PCI Compliance Requirements for Merchants

In 2018 British Airways leaked 400,000 customer records, costing $26 million in fines. Fines aren’t…

Understanding about Front Desk

Front Desk is considered as a simple Property Management System specially designed for small and…

Understanding about Hotel Website

A hotel website is a great way to showcase what kind your business offers. They…